Table of Contents

In India, most people understand health insurance. You pay a monthly premium. If you go to the hospital, the company covers the costs. It sounds simple enough. But for most of us, the moment we actually sit down to buy a policy, a wave of real-world worries hits us.

We start thinking about the people and the “what-ifs” that keep us up at night:

- “What about my parents?” They are 60+, and they already have high blood pressure or diabetes. Will any company actually cover them, or will the “fine print” leave us alone when they need care the most?

- “What if the money runs out?” If I have a ₹5 Lakh policy and a major surgery costs ₹7 Lakh, who covers the extra? What if two family members get sick in the same year?

- “What about the ‘big’ diseases?” We all fear names like cancer or chronic kidney issues. If a disease lasts for years, will the insurance pay the second time? Or the third? Or will they call it a “pre-existing condition” and walk away?

These aren’t just technical questions. They reflect the worries of everyday people who want to secure their family’s future. The truth is, “General Health Insurance” is just the tip of the iceberg. To protect your savings, know that each problem needs its own shield.

In this guide, we are going to clear the confusion. We’ll explore the Types of Health Insurance in India. This includes Senior Citizen plans, and Critical Illness covers. You can stop worrying about “what-ifs” and start feeling secure.

Let’s break it down.

Different Types of Health Insurance: A Comparative Table

Health insurances come in many forms which are suitable for different persons with different health conditions and risk profiles.

Here is a comparative table of which type of health insurance suits whom:

| Type | Suitable for | Features | Benefits | Drawbacks |

| Individual Health Insurance plan | Individuals seeking personalized coverage | Tailored policies, comprehensive coverage | Customisable plans, no-dependence on employer coverage | Potentially higher premiums but depends on age and fitness levels |

| Group Health Insurance Plans | Employees, members of an organisation/association | Collective coverage, cost-effective | Lower premiums, broader coverage | Limited customisation |

| Family Floater Health Insurance Plan | Families | Shared coverage among family members | Cost-effective, single premium payment | Limited coverage for individual family members |

| Senior citizen health insurance | Individuals over 60 years of age | Tailored to senior health needs | Specialised coverage, lower waiting periods | Higher premiums |

| Critical illness plans | Individuals that have a family history or anticipate any critical illnesses | Lump-sum payout on diagnosis | Financial protection against severe illnesses | Limited scope of coverage |

| Top-up Health Insurance | Individuals with existing coverage | Additional coverage after exhausting base policy | Cost-effective, increased coverage | Higher deductibles |

| Maternity Health Insurance | Expecting couples | Coverage for maternity-related expenses | Financial support during pregnancy | Waiting periods, limited coverage |

| Disease-specific insurance covers | Individuals with specific health concerns | Coverage for particular illnesses | Tailored protection | Limited overall coverage |

| Daily hospital cash cover | Individuals seeking daily hospital cash benefits | Daily cash allowance during hospitalisation | Additional financial support | Limited scope of coverage |

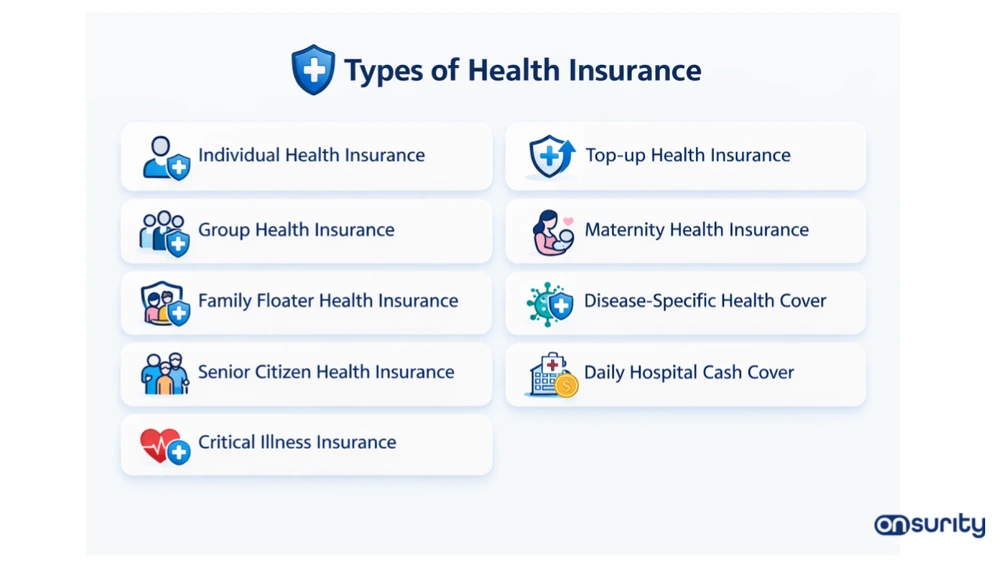

Types of Health Insurance Plans in India

1. Individual Health Insurance Plan

Individual Health Insurance is a personalised safety net, crafted for individuals seeking direct health insurance coverage for a certain policy term. It stands as a shield for those without employer plans or the self-employed, offering autonomy in healthcare choices.

With customizable policies, it provides comprehensive coverage for medical expenses, in-patient costs, from surgeries to diagnostic tests. The benefits include the flexibility of tailoring plans to specific needs and maintaining coverage independently of employment changes. While premiums may be slightly higher, the trade-off lies in personalised and uninterrupted health security.

2. Group Health Insurance

A Group Health Insurance plan is a collective safeguard designed for employees within an organisation. This type of coverage provides a unified and cost-effective solution, spreading financial protection across a group. Typically sponsored by employers, Group Health Insurance ensures that employees benefit from broader coverage at lower premiums.

While customisation options may be limited compared to individual plans, the advantages lie in the shared financial responsibility and accessibility to healthcare benefits. The real strength of Group Health Insurance emerges in its ability to foster a healthier workforce and contribute to the overall well-being of the organisation.

However, new-age insurtechs like Onsurity are changing the norm by offering tailor-made plans based on the size and needs of businesses.

3. Family Floater Health Insurance

Family Floater Health Insurance is a comprehensive safety net designed for families, offering collective coverage for all members under a single policy. This type of plan is a cost-effective solution, streamlining healthcare protection for spouses, children, and sometimes even parents.

With a single premium payment and high sum assured, families gain the advantage of shared coverage, ensuring that each member has access to medical support when needed. While individual needs are considered, the overall emphasis is on providing a cohesive and affordable health insurance solution for the entire family.

In real-life scenarios, Family Floater plans exemplify financial prudence, ensuring that the health and well-being of loved ones is prioritised.

4. Senior Citizen Health Insurance

Senior Citizen Health Insurance is a tailored safeguard meticulously crafted for the unique healthcare needs of elderly individuals. Specifically designed to address age-related health concerns, this plan offers comprehensive coverage for medical expenses in the golden years.

With features such as lower waiting periods in health insurance and specialised coverage, it ensures that seniors receive the care they deserve without undue financial strain. In real-life scenarios, individuals in their senior years find solace and support in a plan that recognizes and caters to their distinct health requirements.

5. Critical Illness Plans

Critical Illness Insurance is a robust financial shield designed to specifically address the challenges posed by severe medical conditions. This plan provides a lump sum payout upon diagnosis of critical illnesses, offering a crucial financial buffer during times of immense health strain.

Tailored to cover major health crises like cancer, heart attacks, kidney failure, and strokes, this insurance plan ensures that policyholders can focus on recovery rather than financial burdens. While the coverage is disease-specific, the benefits of substantial financial support and peace of mind in the face of life-altering illnesses make Critical Illness Insurance an indispensable part of comprehensive health insurance cover.

Also, Read: Domiciliary Hospitalisation Meaning

6. Top-up Health Insurance

Top-up Health Insurance is a strategic add-on supplement to your existing health coverage, providing an extra layer of financial protection when the need arises. This plan comes into play when your primary health insurance limit is exhausted, ensuring extended coverage without a substantial increase in premiums.

With higher deductibles, top-up plans offer a cost-effective solution, allowing you to customise your coverage according to your specific needs. While it complements existing plans, the real advantage lies in the increased financial safety net, offering peace of mind and comprehensive protection against unexpected medical expenses.

7. Maternity Health Insurance

Maternity Health Insurance is a specialised plan designed by insurance companies to embrace the joyous yet financially demanding journey of parenthood. Tailored for expecting couples, this plan provides insurance coverage for pregnancy-related expenses, ensuring that the arrival of a new family member is met with financial confidence.

With features such as coverage for prenatal and postnatal care, delivery, and sometimes even newborn care, Maternity Health Insurance alleviates the financial burden associated with bringing a child into the world.

While it may involve waiting periods, the benefits of securing the well-being of both the mother and the newborn make Maternity Health Insurance an essential investment for those embarking on the beautiful path of parenthood. Buyers should also take care of the room rent limit before making plans.

8. Disease-specific Health Insurance

Disease-specific health insurance policies cover the treatment of only a single disease, such as heart illness, hypertension, cancer, diabetes, AIDS, etc. However, there are specific waiting periods associated with each disease.

The plan covers pre- and post-hospitalization expenses, daily cash, ambulance cover, and health checkups, among other benefits.

Since the coverage is for a single disease, the premium for such plans is usually less. These insurances are usually taken by people who have a risk of inheriting specific health-related issues.

9. Daily Hospital Cash Cover

Hospital Daily Cash Cover is a unique health insurance plan where insurance companies provide financial assistance during hospitalisation, ensuring you have additional support beside the sum insured (under the regular health insurance plan) to manage incidental expenses.

This plan provides a fixed daily cash allowance, allowing you to cover non-medical costs such as transportation and meals while you or your loved ones are receiving hospital care. Though it doesn’t directly cover medical bills, the extra financial cushion eases the burden during times of health crises.

Indemnity and Fixed Benefit Plans

1. Indemnity Health Insurance Plan

Indemnity plans provide the reimbursement of the actual medical expenses incurred through a lump sum amount. They provide flexibility in choosing healthcare providers but may require upfront payment unless hospitalised in a network hospital. Some variations might also be known as mediclaim policy.

2. Fixed Benefit Health Insurance Plan

Fixed benefit plans offer a pre-determined lump sum on the occurrence of specific events or illnesses, irrespective of the actual expenses incurred. While they provide certainty, they may not cover all expenses. Critical illness plans are typically fixed-benefit plans.

Importance of Buying Health Insurance

- Financial Protection: Shields against unexpected medical expenses

- Access to Quality Healthcare: Ensures access to the best medical facilities, without the need for an upfront payment when hospitalised in a network hospitalisation.

- Safeguarding Savings: Prevents depletion of savings during medical emergencies.

- Tax Benefits: Premiums paid towards health insurance are eligible for tax deductions through tax laws such as under Section 80D of the Income Tax Act.

Benefits of Health Insurance Plans

- Comprehensive Coverage: All-encompassing protection against various medical expenses even if in crores.

- Peace of Mind: Assurance of financial support during health crises.

- Preventive Medical Care: Encourages regular health check-ups and preventive measures to diagnose health issues at an early stage.

- Network Benefits: Access to a wide network of healthcare providers

- Little to no out-of-pocket expenses.

Things to Consider While Choosing Health Insurance Plans

1. Coverage Needs

Assess both individual and family healthcare needs by considering existing medical conditions, potential future requirements, and the overall medical history. This comprehensive evaluation ensures that the selected health insurance plan adequately addresses the specific health concerns of all members covered.

2. Affordability

Evaluate the premiums and benefits offered by different health insurance plans in accordance with budget constraints. Striking a balance between cost and coverage is essential to ensure that the chosen plan remains financially sustainable over the long term.

3. Network Hospitals

Confirm the availability of preferred healthcare providers within the insurers’ network. This step ensures convenient access to quality medical care and minimizes out-of-pocket expenses when seeking treatment from network hospitals.

4. Waiting Periods

Understand the waiting periods associated with specific coverages within the health insurance plan. Waiting periods can vary for different treatments or conditions, and being aware of these details helps manage expectations and plan for potential healthcare needs accordingly.

5. Exclusions

Scrutinise policy exclusions, terms, and conditions to avoid surprises at the time of making claims. A thorough understanding of what is not covered by the insurance policy is crucial to prevent any misunderstandings or unexpected financial burdens during medical emergencies.

6. Accident Insurance

Check if the health insurance policy includes provisions specifically tailored to personal accidents. Having coverage for accidents ensures additional financial protection in case of unforeseen events resulting in injuries, offering peace of mind and comprehensive coverage.

7. Pre and Post-Hospitalisation Expenses

Emphasise the coverage for pre and post-hospitalisation expenses. Recognise the importance of extending coverage beyond the actual hospitalisation period, as the costs of medical treatment often extend before admission and after discharge.

Ensuring comprehensive coverage for these phases contributes to a more robust and holistic health insurance plan.

Conclusion

At the end of the day, health insurance isn’t just about hospital bills or tax deductions. It’s about seeing your aging parents, your kids, and your savings, and knowing they’re all secure.

In a country where medical costs rise by 14% each year, the “one-size-fits-all” insurance model is outdated. The confusion about chronic diseases, coverage limits, and elderly care is real. But it can be solved. You can choose a Senior Citizen plan for your parents, or Critical Illness cover for major health concerns. There’s a shield for every worry.

Don’t wait for a medical emergency to discover if your policy is sufficient. Take 15 minutes today to review your current coverage. Ask tough questions now. When life throws a curveball, focus on what matters: getting better.

Don’t let the fine print hold you back. If you’re unsure which plan suits your family.

Ready to take the next step?

FAQs

1. Why do you need a health insurance policy?

Medical inflation in India is nearly 14% each year. Because of this, a single hospital stay can erase years of savings. Health insurance is a form of financial security. It helps you get quality care, so you can stick to your goals without spending too much.

2. How to purchase health insurance in India?

You can buy a policy in several ways:

a) Directly from an insurer’s website.

b) Via a licensed agent

3. How does smoking affect health insurance premium?

Insurers see smokers as “high-risk.” This is because they are more likely to have respiratory and heart problems. Smokers may face premiums 20-40% higher than non-smokers. It’s important to share this information to prevent claim rejection later.

4. How to port a medical insurance policy?

You can “port” or switch your insurer under IRDAI rules. This way, you won’t lose the “waiting period” benefits you’ve earned. Apply to the new insurer at least 45 days before your current policy ends. This gives time for your medical records to transfer.

5. What are the various types of health insurances?

In India, the main types of health insurance are:

a) Individual Health Insurance: Covers one person’s medical expenses.

b) Family Floater Plan: Shared cover for entire family.

c) Senior Citizen Insurance: Specialized care for age 60+.

d) Critical Illness Cover: Lump-sum payout for major diseases.

e) Maternity Insurance: Covers pregnancy and newborn care.

f) Group Health Insurance: Employee coverage provided by companies.

g) Personal Accident Insurance: Payout for accidental death/disability.

h) Disease-Specific Plan: Targeted cover for Diabetes/Cancer.

i) AYUSH Insurance: Covers Ayurveda and Homeopathic treatments.

6. What are the four most important types of insurances?

To reach full financial security, experts suggest getting:

a) Life Insurance (Term Plan)

b) Health Insurance

c) Critical Illness Insurance

d) Personal Accident Insurance

7. What are the top three health insurances?

The “best” plans depend on your needs. Right now, the top-rated options in India include:

a) Comprehensive Family Floater Plans

b) Individual or Personal Health Insurance

c) Specialized Plans for Senior Citizens

d) Group Health Insurance

8. What is the most common type of health insurance?

The Individual plan and Family Floater Plan is the most popular choice in India. It’s very cost-effective. It covers the policyholder, spouse, and children under one “shared” sum insured. This makes it cheaper than buying separate policies for each person.

9. What are the two basic types of insurance?

Insurance is mainly split into two types:

a) Insurance: This pays out when someone dies.

b) General Insurance: This covers things like assets and health. Examples include medical, motor, and home insurance.

Clinical Content Strategist B.Pharma

A Senior Medical and Insurance Content Strategist with over 6 years of experience in healthcare, Ayurveda, and insurance, Diksha has written for industry leaders such as Onsurity, Tata 1mg, mfine, and Medi Assist. A Bachelor of Pharmacy graduate and the creator of the Insurance Dictionary; she holds a Professional Diploma in Counseling Psychology and is certified in Counseling and Guidance by the International Psychological Association.